.jpeg)

In my recent article on the One Big Beautiful Bill (OBBB), I shared how Congress just made one of the most valuable small business deductions permanent — the 20% Qualified Business Income (QBI) deduction under Section 199A.

For S corporation owners, this change is more than good news — it’s a reason to revisit your reasonable compensation strategy.

Why? Because once you cross the QBI income threshold, your deduction is limited by the greater of:

- 50% of W-2 wages, or

- 25% of W-2 wages + 2.5% of unadjusted basis in qualified property (UBIA)

That means your officer salary — the W-2 wages you pay yourself — plays a direct role in whether you get the full 20%deduction, a partial deduction, or nothing at all.

5 Planning Moves for S Corp Owners

1. Set W-2 Wages at True Reasonable Compensation

The IRS requires S corp owners to pay themselves a reasonable salary for the work they perform before taking distributions. This salary should be based on objective criteria — like your role, responsibilities, experience, hours worked, and industry standards — not just a number that “feels right.” Once your reasonable compensation is established, you can see how that wage level interacts with the QBI wage limitation to protect both compliance and your deduction.

2. Time Income and Deductions

If you’re near the QBI phase-out threshold, strategically shifting when you recognize income or deductions can preserve more of the 20% benefit. Just remember — your reasonable compensation still needs to be paid in full for the year, regardless of timing strategies.

3. Separate SSTB from Non-SSTB Activities

Specified Service Trades or Businesses (SSTBs) face tighter QBI limits. If part of your work is SSTB and part is not, keeping these activities legitimately separate — with distinct records, accounts, and operations — can help preserve the non-SSTB deduction. Reasonable compensation applies separately to each Scorp, so don’t overlook wage requirements when separating operations.

4. Aggregate Related Businesses

If you own multiple entities with common ownership and operational interdependence, aggregation can combine QBI, wages, and UBIA to improve the deduction. When aggregating, ensure that reasonable compensation is set appropriately for each S corp within the group — the IRS looks at each entity’s wages, not just the total.

5. Plan Equipment Purchases for UBIA

For those limited by the “25% wages + 2.5% UBIA” formula, placing qualified property into service before year-end can lift the deduction. This can be especially effective for S corps whose reasonable compensation wages alone don’t fully unlock the QBI benefit.

Bottom Line

With QBI now permanent under the OBBB, reasonable compensation planning isn’t just about avoiding IRS penalties — it’s about unlocking an annual 20% deduction. The right salary can mean the difference between keeping that benefit or losing it to the phase-out rules.

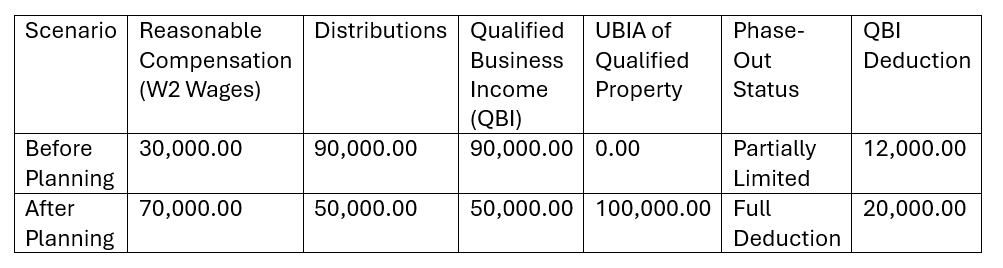

If you want to see how your officer wages affect your QBI deduction, here’s a sample:

QBI Planning Before & After Chart